It’s easy enough to fill up a loan application. But if you’ve ever had a loan rejected before, you’ll know what a real headache that can be! So, what do banks really look for in your loan application? If you really want the banks to open up their vaults for you, here are a few things you need to look out for:

Contents

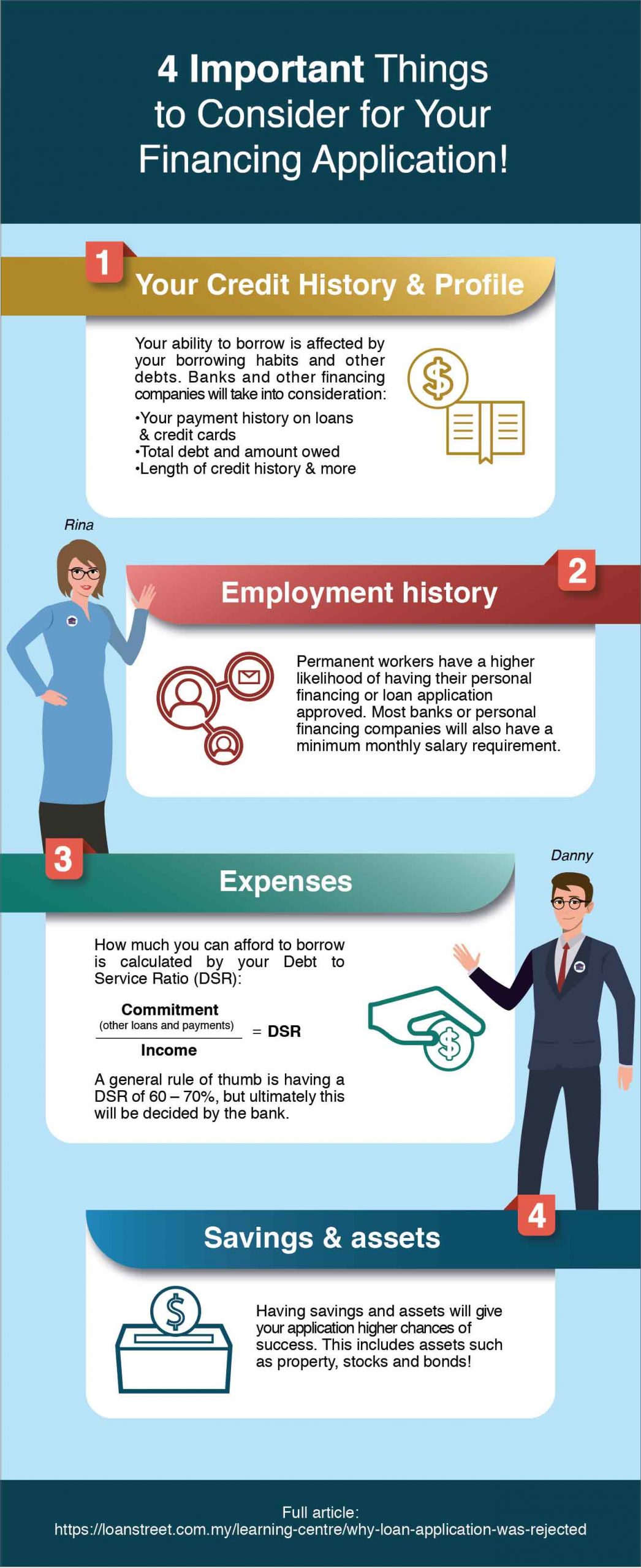

1. Credit history and profile

You might be wondering what a credit profile is, but really, it’s not that different from your Facebook profile. Every single financial action that you’ve taken in your adult life is recorded and tracked by the banks – including your student loan.

The recorded data about your financial history will be continuously updated and when combined, make up your credit profile. The banks will refer to this whenever you apply for a loan or a credit card, and decide whether you’re a ‘safe risk’ (basically if you’re able to pay them back or not) from the stored information which includes:

- Your payment history on loans and credit cards

- Total debt and amount owed

- Length of credit history and more

If you have any past bankruptcies, late payments, or even past rejected loan applications, it will reflect negatively on your credit profile. That’s why you need to take appropriate steps first, like clearing up any late payments, before you submit your loan application.

But, how in the world do you remember your entire credit history? It might surprise you that Bank Negara’s CCRIS and CTOS records every credit-related decision you’ve ever made.

The good thing is that you can have access to them easily; all you’d need to do is register online and pay a small fee to get a copy of your credit history. Read our article, “Everything You Should Know About CTOS” to learn how to do it yourself!

2. Employment History

You don’t need a fancy, high-paying job to get a loan; what you do need is to prove that you’re earning a consistent and stable salary in your employment. For example, it looks better on your credit profile if you’ve worked at a company for longer than a year, compared to a scenario where you’ve switched employment every 3 months.

All banks are upfront about their minimum monthly salary requirement, so make sure you check if what you’re earning is indeed eligible for the loan amount that you want to apply for. Also, remember that banks are all about the black and white, so make sure to always get a valid payslip from your employer, even if he/she prefers to pay in cash!

3. Expenses

Don’t think that just because you’re earning a higher-than-average salary, you’re automatically eligible for a loan. What banks really look for is your debt servicing ratio (DSR). In other words, banks want to know EXACTLY how much you have left over after deducting all of your total expenses. In that way, they’re able to see if you can afford to pay them back later. Here’s a simplified version of the DSR calculation:

DSR = Commitment / Income

The general rule of thumb is that you need to keep your DSR around 60-70%, but bear in mind that the final rate would really be decided by your bank of choice. Let’s take an example to see how it’s calculated. So, let’s say you earn RM6,000 a month; you spend RM600 on the car loan, RM1,000 on the mortgage, RM1,200 on the student loan, and another RM1,500 on credit cards repayment. Your total expenses would make up RM4,300.

RM4,300 / RM6,000 x 100% = 71.67%

As you can see, your DSR is already past the mark! If you already have too much on your plate, the banks might look at you as a ‘high-risk’ borrower and not approve your loan application.

4. Savings and Assets

Having a comfortable pool of savings and assets (such as property, stocks, and bonds) will give your loan application more chances of success. It tells your bank that you’re able to cover your loan repayments in case of a financial setback. You may also be given a lower interest rate with a difference of 0.05-0.1% which will make a lot of difference in your monthly payments over the loan duration.

What can you do now?

The key to getting your loan application accepted is to plan ahead and do thorough research. A good financial profile takes years in the making. If you’d like a head-start in finding out whether you’re on the right track, why not make use of Loanstreet’s free loan comparison tool to search and compare all products to find the best fit for you!

Or better yet, if you’re working with the government or GLCs, you can get exclusive financial assistance up to RM150,000 from YIR for faster approval – within 2 working days. YIR is solely funded by RCE Marketing Sdn Bhd (“RCEM”) through a partnership agreement. RCEM is a subsidiary company of RCE Capital Berhad, an investment holding company incorporated in Malaysia and listed on the Main Market of Bursa Securities on 23 Aug 2006.

On top of that, they also offer profit rates as low as 6.50% to 9.99% p.a., which is better than the industry average rate of 8%.

Good luck!